When it comes to background checks, this mantra can save your organization from severe legal consequences: Know the rules, then choose the right tool. The Fair Credit Reporting Act (FCRA) imposes strict requirements on certain types of background screening, but not every situation falls under its umbrella.

In some cases, a non-FCRA background check (one not governed by the FCRA) is not only perfectly legal but also a more strategic and flexible option for deeper due diligence.

As litigation is on the rise and regulators are paying closer attention to employer screening practices, understanding your legal obligations under the Fair Credit Reporting Act (FCRA) has never mattered more.

With an understanding of the distinctions between FCRA and non-FCRA background checks, compliance teams and risk officers get the information they need without unnecessary exposure, and that’s what we’re going to cover today.

Below, we break down when FCRA compliance is mandatory, when a non-FCRA approach makes sense, and why the right choice is such an important decision.

The Fair Credit Reporting Act (FCRA) is a U.S. federal law passed in 1970 to promote the accuracy, fairness, and privacy of consumer information in the files of consumer reporting agencies.

In simple terms, the FCRA protects consumers from having their personal “consumer reports” (e.g., credit reports or background reports) used against them without their knowledge.

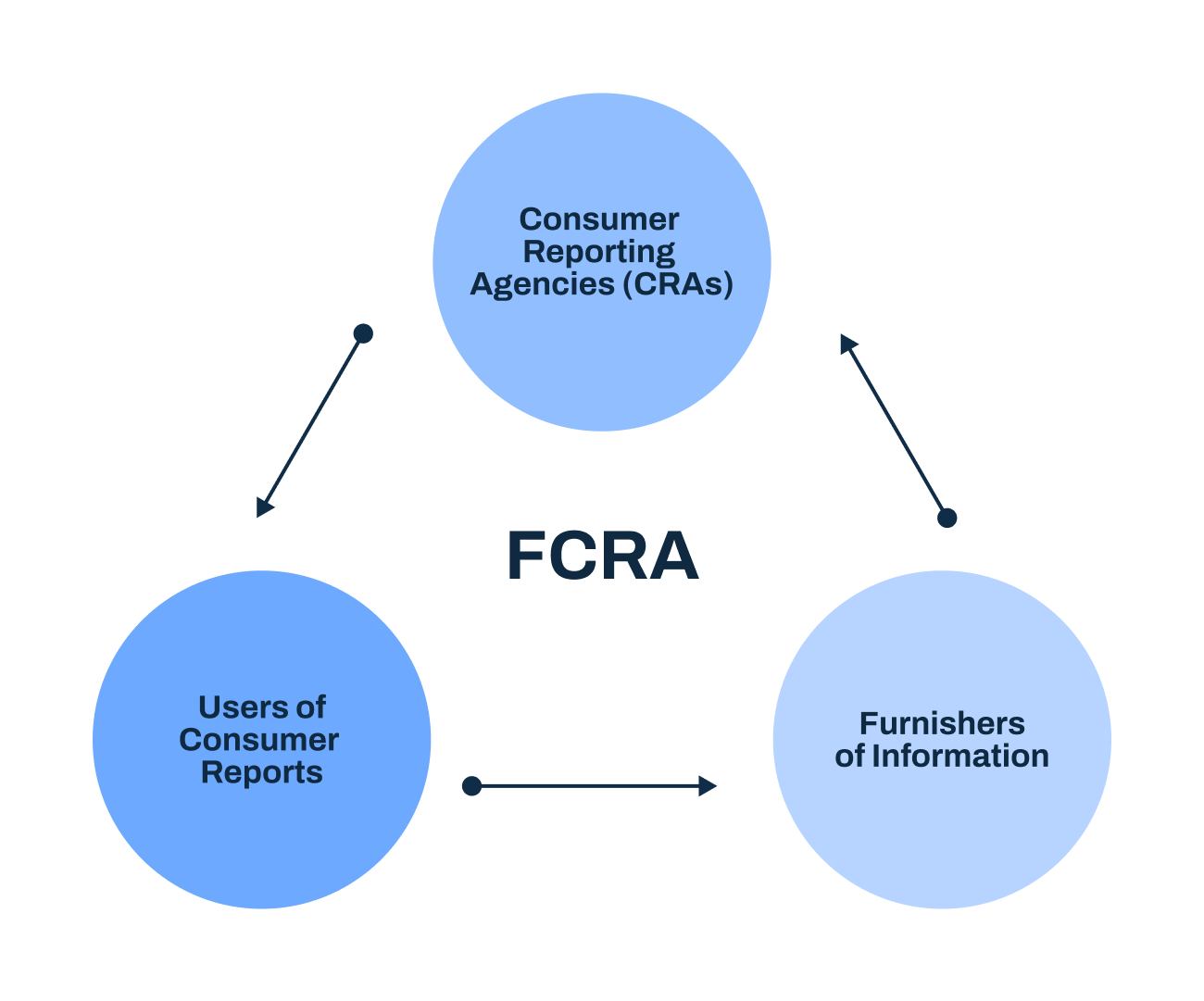

To achieve this, the law regulates three key groups:

Under the FCRA, a “consumer report” includes any communication of information by a CRA bearing on a person’s credit, character, reputation, personal characteristics, etc., used to determine eligibility for purposes like credit, insurance, employment, or housing.

In fact, the law spells out specific “permissible purposes” for which a CRA may furnish a report, and we’ll discuss some of those in a moment.

Why does this matter? FCRA compliance carries significant responsibilities and potential liabilities. Users of FCRA-regulated reports must provide pre-adverse action notices and adverse action notices if they decide not to hire or approve someone based on a report, giving the individual a chance to review and dispute the findings.

They must also ensure they only access reports for a permissible purpose and follow data retention and privacy rules. Failure to comply can lead to lawsuits, regulatory penalties, and even class action exposure.

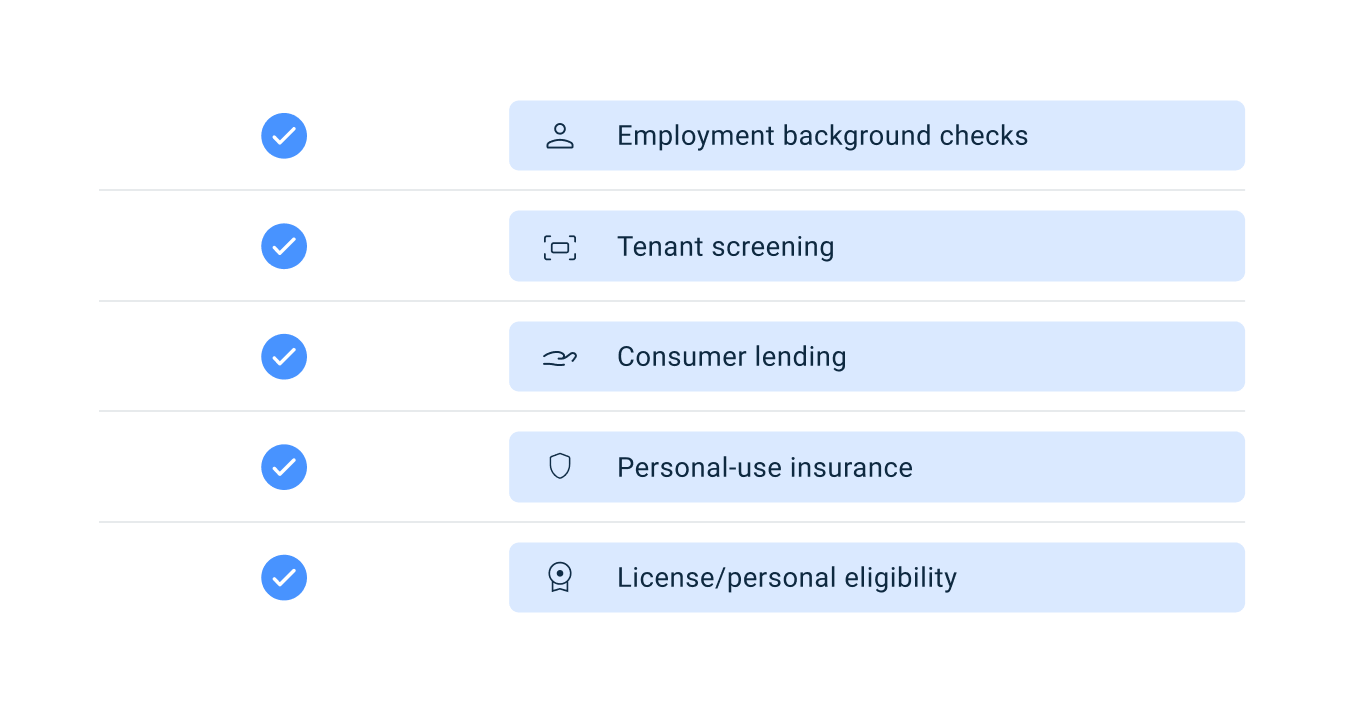

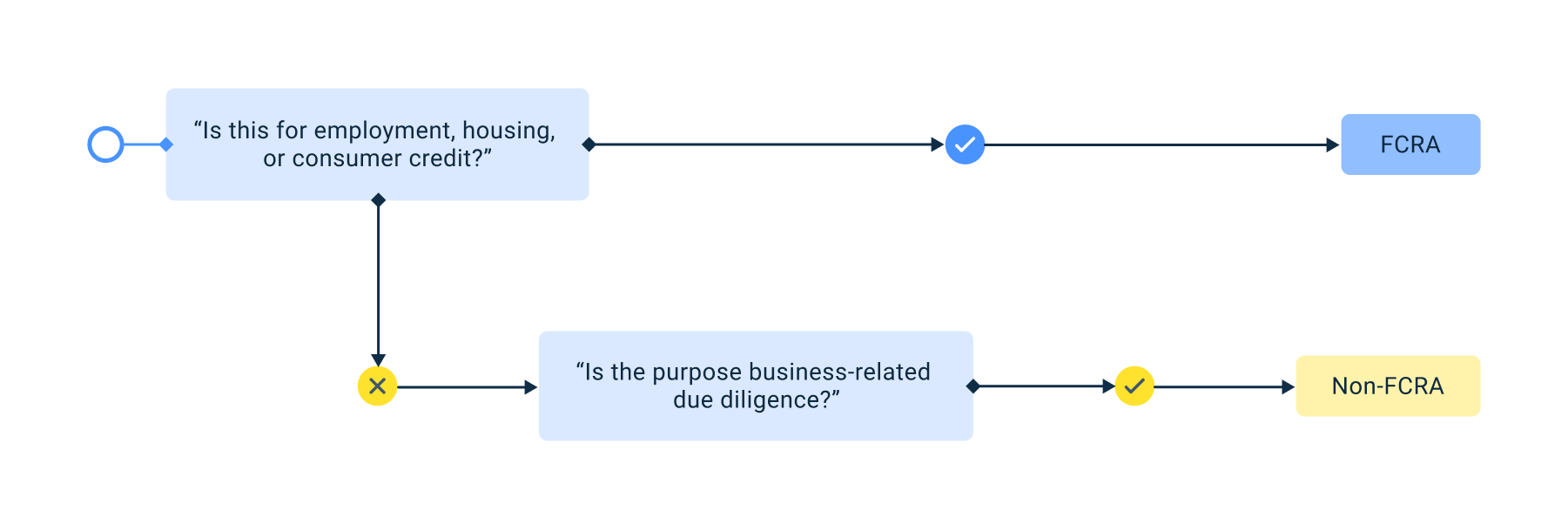

Next, let’s clarify some of the use cases that unequivocally require an FCRA-compliant background check (and thus trigger all of the law’s requirements):

In all of these cases, you must use an FCRA-compliant process and provider. That means using a reputable consumer reporting agency that follows FCRA procedures (e.g., verifying data accuracy and providing mandated notices) and ensuring your own internal processes meet the law’s requirements.

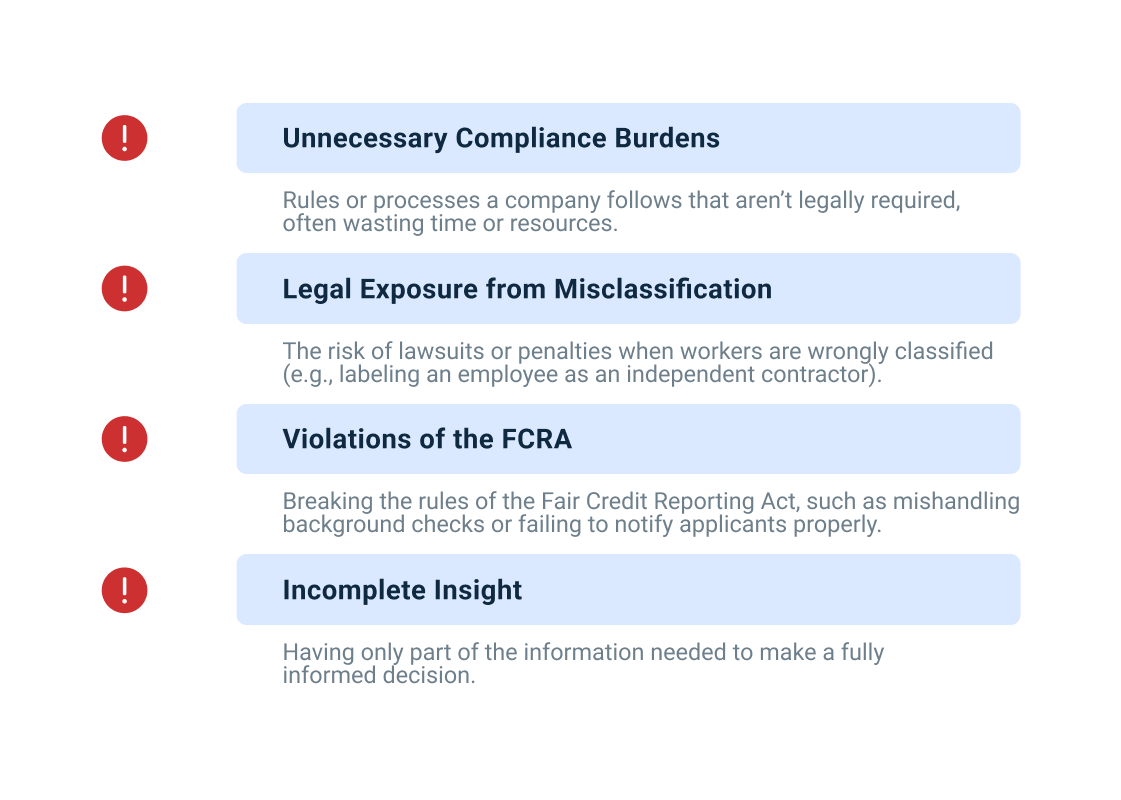

Not all background checks fall under the same legal umbrella, and choosing the wrong one can be a costly mistake.

A non-FCRA background check refers to any background screening or investigation that is not being conducted for the FCRA-defined purposes of employment, consumer credit, insurance, or tenancy, and thus is not subject to the FCRA’s procedures.

Crucially, a non-FCRA check is not meant to determine an individual’s eligibility for a job, personal loan, or housing; instead, it’s often used for risk management, fraud prevention, or commercial due diligence.

Many of the same types of records used in an FCRA report (court records, criminal history, liens, etc.) can also be used in a non-FCRA context. The difference lies in how the information is used and who the end user is.

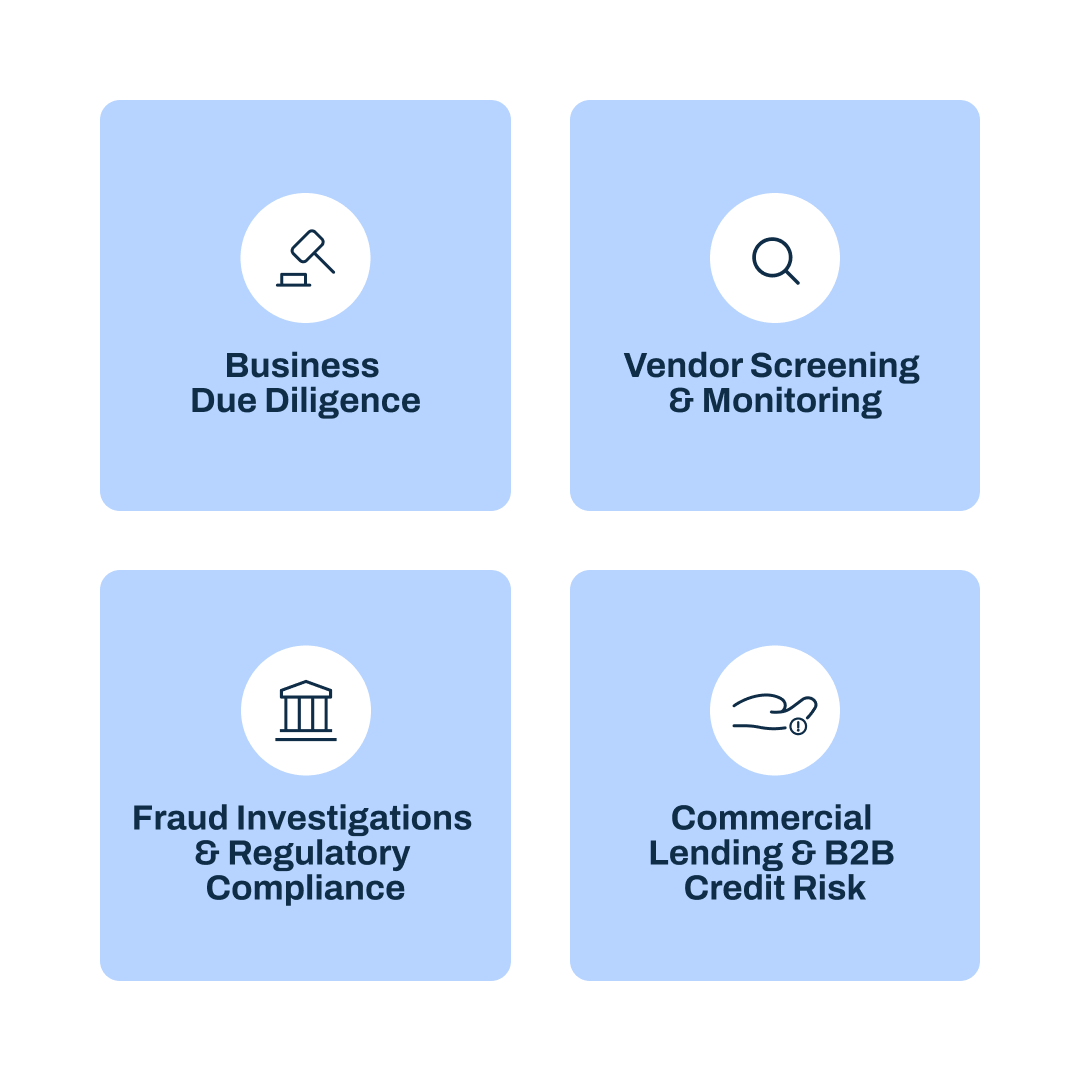

Any check that is solely on a business is a non-FCRA background check. Here are a handful of common scenarios where non-FCRA background checks are preferred or legally appropriate:

Non-FCRA checks offer clear advantages when used appropriately. Without FCRA’s procedural steps, they provide broader insight, pulling from sources like international records and media.

Since these checks aren’t used for employment or personal credit decisions, they typically don’t require consent or notices, so the process can be faster and more discreet.

Importantly, using a non-FCRA service does not mean anything goes. Reputable non-FCRA providers still adhere to privacy and permissible use laws to prevent misuse of data.

It’s an understandable caution to think it’s best to default to FCRA if in doubt. However, it can be counterproductive and even risky to default to FCRA checks when they’re not required.

Here’s why:

If you treat a business partner or high-net-worth client like a job applicant, you may need to request written consent and share the report if you opt not to move forward. Non-FCRA Reports can be run discreetly without consent and speed up due diligence processes.

That’s not typical in B2B settings and can disrupt candid evaluations. Using an FCRA report when it isn’t required adds unnecessary hurdles and can slow down decisions that would otherwise be routine.

Using an FCRA background check in the wrong context can backfire. Independent contractors are a good example: while the law mentions “employment,” contractors aren’t technically employees.

Misusing FCRA can lead to unintentional violations. Claiming a permissible purpose that doesn’t apply, such as “employment” for someone who won’t be an employee or “credit” with no loan involved, is a breach of the law.

Both the requester and the CRA can be held responsible for pulling a report without a valid reason.

FCRA checks often leave out details that matter in non-consumer contexts. To comply with the law, they typically exclude older records, such as civil lawsuits over seven years old or bankruptcies over 10. But if you’re assessing a business partner, a 12-year-old bankruptcy might be important.

In summary, it’s not “safer” to over-apply FCRA in every scenario.

Misclassifying a background check can open the door to lawsuits, regulatory penalties, and reputational damage.

To drive home the importance of choosing correctly, let’s look at a few examples of how missteps in this area can lead to trouble:

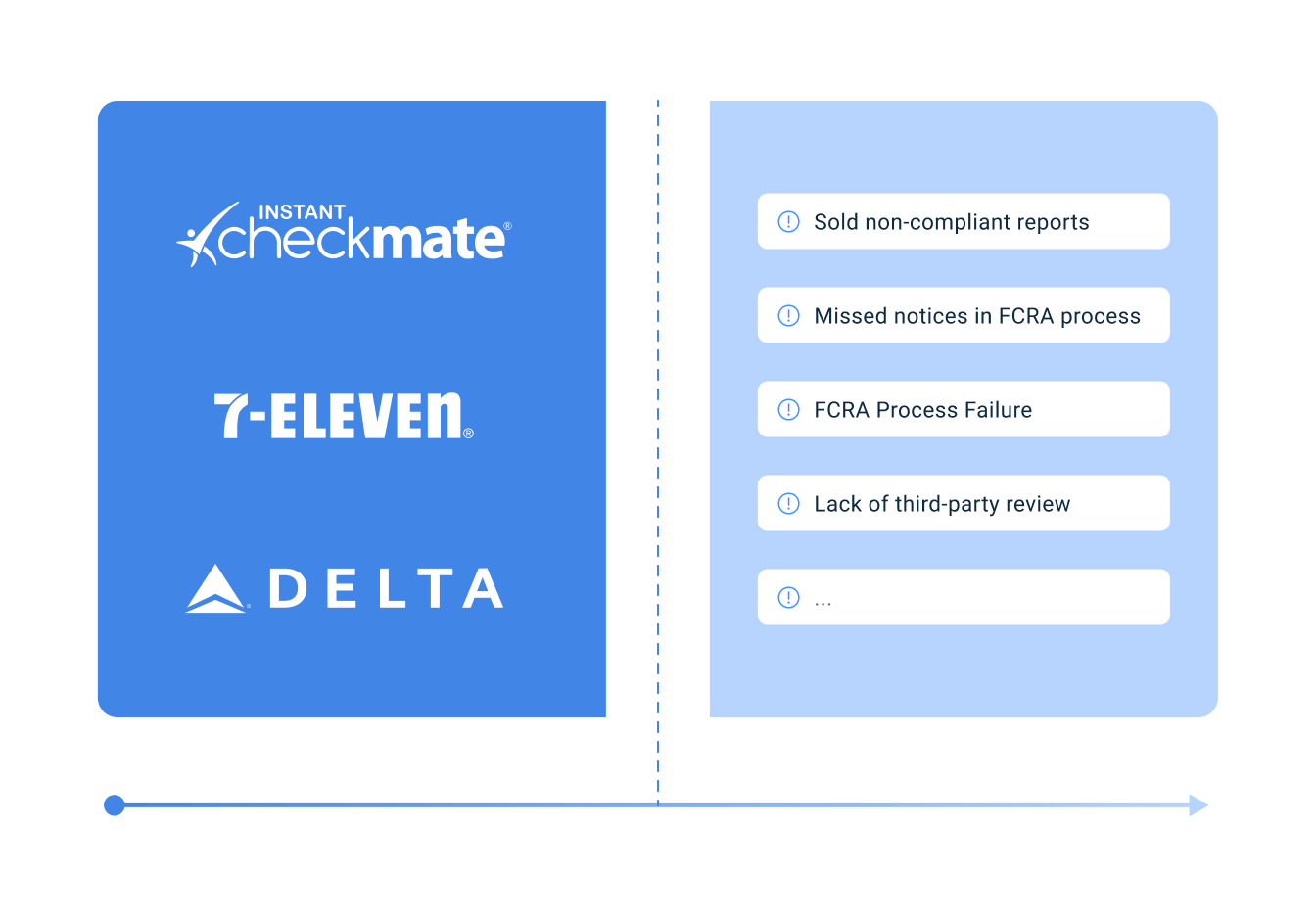

A manager might try to save money using a cheap people-search site or app to vet a job candidate instead of ordering a proper FCRA-compliant background check.

But what if that service provides information used in an employment decision? Then it qualifies as a consumer reporting agency. If it isn’t following FCRA, both the service and the employer can be liable.

The FTC has taken action against companies like Filiquarian and Instant Checkmate for marketing these kinds of reports to employers without meeting FCRA requirements. The takeaway: the fines for using non-compliant services for employment decisions can far exceed any savings.

Another common mistake is assuming you’re fully compliant with FCRA, but overlooking a fundamental step.

FCRA claims against employers have surged in recent years, often tied to missed notices or flawed disclosure forms. If your team handles hiring, routinely review your process.

For example, 7-Eleven and Delta Airlines have faced class action lawsuits costing them over $2 million each, not for running background checks improperly, but for missing key FCRA steps.

The above examples underscore that using consumer data carries responsibility. Whether under FCRA or not, ethics and accuracy matter.

Given the legal and operational consequences of misclassifying background checks, choosing a screening provider who understands the differences between FCRA and non-FCRA background checks isn’t a decision to make lightly.

Understanding the nuances of these background checks is not easy, and that’s where choosing the right partner becomes paramount. Business Screen specializes in non-FCRA background checks for the commercial lending, real estate investment, vendor, and third-party screening, as well as financial services sectors.

At Business Screen, we pride ourselves on being a knowledgeable and ethical partner in this space. We respect the FCRA, and when a check should be FCRA-compliant, we’ll tell you so and won’t cut corners.

But when a non-FCRA check is the smarter choice, we have the tools and expertise to deliver broader information quickly and securely.

Our reports are compiled by licensed investigators and include human-vetted insights, not just raw data. That means you get actionable information (not mountains of search results) to make informed decisions with confidence.

Always consult with your legal/compliance team before proceeding with any background check program – this cannot be overstated. We work hand-in-hand with our clients’ compliance officers to ensure each screening program is designed correctly.

Need advice tailored to your specific scenario?

Book a free consultation with Business Screen. We’ll help you navigate these requirements and craft a screening solution that fits your needs, helping you stay on the right side of the law while gaining the insights that matter.

.png)