Understand kyb and kyc verification differences. Protect your business from fraud & fines with expert due diligence. Learn best practices now!

KYB and KYC verification are two essential processes that help businesses identify and verify their customers and business partners to prevent financial crime and ensure regulatory compliance.

Quick comparison:

Nothing thrills — or terrifies — a compliance professional more than navigating complex verification requirements. As one compliance analyst noted, dealing with "multiple layers, the seemingly random presence of holding companies, dotted and solid lines of indirect ownership" makes these processes both critical and challenging.

The stakes couldn't be higher. In 2019 alone, banks received $10 billion in fines, with over 60% for failing to comply with anti-money laundering regulations. More recently, Bancrédito International Bank was fined $15 million by FinCEN for inadequate verification programs.

I'm Ben Drellishak, and I've spent years helping businesses steer the complexities of KYB and KYC verification through comprehensive risk assessments and due diligence investigations. My experience has shown me that understanding these verification processes is crucial for protecting your business from financial crime and regulatory penalties.

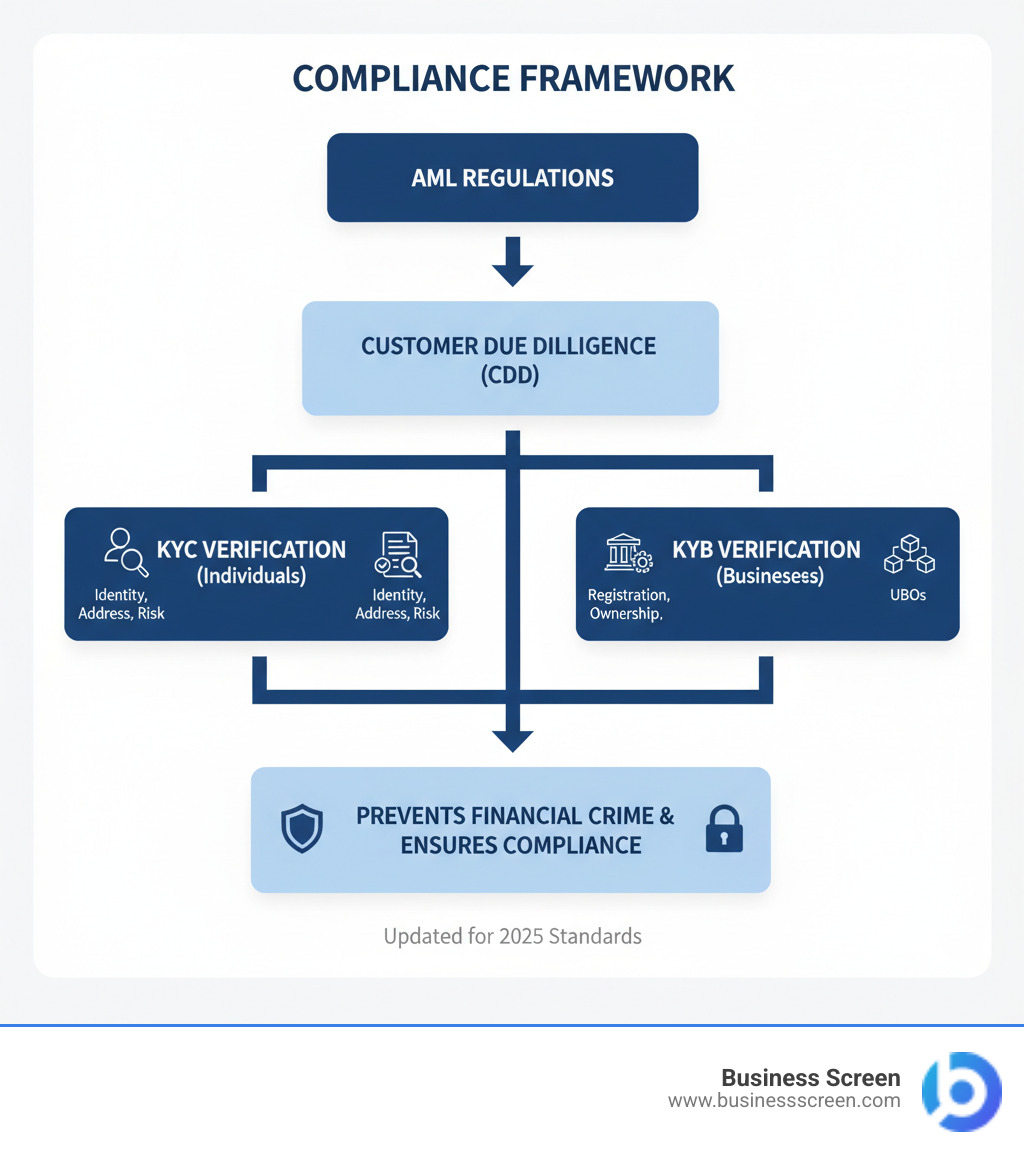

Before we dive into the nuts and bolts of KYB and KYC verification, let's clear up what these acronyms actually mean. Both processes fall under the broader umbrella of Customer Due Diligence (CDD) — think of it as your business's detective work to understand who you're really dealing with.

KYC stands for "Know Your Customer" and focuses on verifying individual people. When someone wants to open an account or do business with you, KYC helps you confirm they are who they say they are. It's your first line of defense against identity theft and fraud.

KYB means "Know Your Business" and does the same thing for companies. When another business wants to partner with you, KYB verification helps you understand whether that company is legitimate or potentially a front for something shady.

Both processes serve the same fundamental purpose: preventing financial crime. They help you spot red flags early, comply with regulations, and protect your business from becoming an unwitting accomplice to money laundering or other illegal activities.

The beauty of these systems is that they create a safety net for the entire financial system. When businesses properly verify their customers and partners, everyone benefits from reduced fraud and increased trust. For a deeper dive into how these programs work, check out our guide on Accurate Customer Identification (CIP) & Know Your Client (KYC) Background Check Programs.

When you're getting to know a new individual customer, KYC verification follows a pretty straightforward path. It starts with collecting basic information and progressively builds a complete picture of who they are and what risks they might pose.

Personal data collection forms the foundation of any KYC process. You'll gather their full name, date of birth, address, and contact details. But collecting information is only half the battle — you need to verify it's accurate.

Individual identity verification typically requires official documents. Most businesses ask for a passport or driver's license to confirm identity, plus a recent utility bill to verify their address. These documents help ensure the person standing in front of you (or applying online) matches the information they've provided.

Risk assessment is where things get more interesting. Not every customer poses the same level of risk to your business. Someone applying for a basic service from a low-risk country will need less scrutiny than a Politically Exposed Person (PEP) — individuals who hold prominent public positions and might be more susceptible to corruption.

Ongoing monitoring rounds out the KYC process. This isn't a one-and-done deal. You'll continuously watch for unusual activity or changes in your customer's circumstances that might signal problems. Think of it as keeping your finger on the pulse of your customer relationships.

The goal is simple: make sure you know who you're doing business with and that they're not using your services for illegal purposes. It protects both your business and your legitimate customers from becoming victims of financial crime.

KYB verification is like KYC's more complicated cousin. While individual verification is relatively straightforward, businesses can have complex ownership structures that make figuring out who's really in charge a genuine puzzle.

Business entity verification starts with the basics. You'll confirm the company is properly registered by checking with official sources like Companies House in the UK or similar government registries elsewhere. This includes verifying their legal name, registration number, and current status.

Corporate structure analysis is where things get tricky. Some businesses have simple ownership — one person owns everything. Others have layers upon layers of holding companies, subsidiaries, and complex arrangements that can make your head spin. You need to map out these relationships to understand who really controls the business.

Ultimate Beneficial Owners (UBOs) and Persons with Significant Control (PSCs) are the real people behind the corporate veil. These individuals typically own 10-25% or more of the business or exercise significant control over its operations. Once you identify them, they go through their own KYC process.

This is where things can get challenging. Picture trying to untangle a corporate ownership chart that looks like a spider web — with dotted lines, indirect ownership, and holding companies scattered across multiple jurisdictions. It's enough to give any compliance professional a headache.

The stakes are high because shell companies — businesses that exist only on paper — are favorite tools for money launderers. By thoroughly understanding a company's structure and ownership, you can spot potential red flags and avoid partnerships that might put your business at risk.

KYB verification helps ensure you're dealing with legitimate businesses run by real people with genuine commercial purposes. In today's interconnected business world, this due diligence isn't just smart — it's essential for protecting your reputation and staying on the right side of the law.

While both kyb and kyc verification share the noble goal of preventing financial crime, they're like two different tools in your compliance toolkit - each designed for specific situations. Think of KYC as your magnifying glass for examining individuals, while KYB is more like a complex organizational chart analyzer for businesses.

Understanding these distinctions isn't just academic - it's crucial for building an effective verification strategy that actually works in practice.

The fundamental difference is focus: KYC zeroes in on individual customers - verifying their identity, checking their background, and understanding their personal risk factors. It's relatively straightforward because you're dealing with one person and their documentation.

KYB, on the other hand, tackles the much more complex world of business entities. Here, we're not just looking at a single individual but potentially dozens of people connected to a company through ownership, control, or influence. We need to understand corporate structures that can span multiple countries and involve layers of holding companies.

Complexity levels differ dramatically between the two processes. A typical KYC check might require a passport, utility bill, and risk assessment. But KYB? That's where things get interesting. We might need to trace ownership through multiple jurisdictions, identify Ultimate Beneficial Owners hiding behind shell companies, and understand corporate structures that would make a compliance analyst's head spin.

The information requirements tell the story clearly. For KYC, we're gathering personal details - name, address, date of birth, and identity documents. For KYB, we're collecting business registration details, ownership charts, financial statements, and detailed information about every person with significant control over the company.

Primary goals also differ in scope. KYC aims to prevent individual-level fraud, identity theft, and ensure the person is who they claim to be. KYB has a broader mission - exposing shell companies, understanding complex ownership structures, and ensuring legitimate business relationships.

The business context matters too. KYC typically applies in B2C relationships - when a bank opens an account for an individual customer, for example. KYB comes into play in B2B scenarios - when companies are partnering, acquiring services, or establishing business relationships.

Both processes require ongoing monitoring, but the triggers and complexity differ significantly. Individual customers might change addresses or employment, while businesses can undergo mergers, acquisitions, or complete ownership restructuring.

For a deeper understanding of how these verification processes work together in practice, check out our guide on What is KYB, KYC, and KYCC? Why it Matters.

The bottom line? While KYC and KYB are both essential for compliance, they're addressing different pieces of the financial crime puzzle. Getting both right isn't just about avoiding fines - it's about building a business that operates with integrity and trust in an increasingly complex global marketplace.

The world of kyb and kyc verification operates within a complex web of regulations that can feel overwhelming at first glance. Think of it as a maze where each turn represents a different jurisdiction, each wall a new compliance requirement, and each dead end a potential regulatory pitfall. But here's the thing – understanding this maze isn't just about avoiding penalties; it's about building a business that operates with integrity and earns genuine trust.

What makes this particularly challenging is that regulations aren't one-size-fits-all. What works perfectly in New York might not meet the standards in London, and what satisfies European regulators could fall short in Singapore. Add to this the constantly evolving nature of these rules – new threats emerge, regulations adapt, and businesses must stay nimble to keep up.

Data privacy adds another layer of complexity to the mix. While we're gathering information to prevent financial crime, we must also respect customers' privacy rights. It's a delicate balance between being thorough and being respectful. The General Data Protection Regulation (GDPR) in Europe, for instance, sets strict guidelines on how personal data must be handled, stored, and protected.

The stakes here go beyond just checking boxes. Effective compliance protects your business reputation, keeps you out of legal trouble, and helps maintain the integrity of the entire financial system. For businesses dealing with international partners, understanding these requirements becomes even more critical. Our guide on The Complete Guide to FCPA Compliance offers valuable insights into navigating complex compliance landscapes.

Let's start with the global foundation. The Financial Action Task Force (FATF) serves as the international standard-setter for combating money laundering and terrorist financing. Their 40 recommendations aren't just suggestions – they're the blueprint that countries worldwide use to build their own regulatory frameworks. These recommendations cover everything from customer due diligence to suspicious transaction reporting and international cooperation.

In the United States, several key pieces of legislation shape how kyb and kyc verification must be conducted. The Bank Secrecy Act (BSA) laid the groundwork decades ago, requiring financial institutions to help government agencies detect and prevent money laundering through careful record-keeping and reporting.

The 2001 US Patriot Act significantly strengthened these requirements following the September 11 attacks. This legislation introduced stricter identity verification requirements and improved due diligence measures, particularly for foreign accounts and politically exposed persons.

More recently, the CDD Final Rule issued by FinCEN has clarified and strengthened customer due diligence requirements. This rule explicitly requires financial institutions to identify and verify the beneficial owners of legal entity customers – essentially making KYB verification mandatory for many businesses.

Across the Atlantic, the European Union takes a slightly different but equally rigorous approach. The EU Anti-Money Laundering Directives (AMLDs) provide a comprehensive framework that member states must implement. The Fifth Anti-Money Laundering Directive (5AMLD) introduced improved transparency requirements and expanded the scope of entities that must comply with AML obligations.

In 2021, the EU proposed creating a unified AML rulebook and establishing a new EU Anti-Money Laundering Authority (AMLA). This signals an even stronger push toward harmonized standards across member states, making compliance more predictable for businesses operating across Europe.

The General Data Protection Regulation (GDPR) adds another crucial dimension to compliance considerations. While not directly an AML regulation, GDPR sets strict standards for how personal data collected during KYC and KYB processes must be handled, stored, and protected.

Following Brexit, the United Kingdom has maintained many EU-aligned standards while also adapting to FATF recommendations directly. The UK's money laundering regulations were updated in 2020, creating some unique requirements for businesses operating in British markets.

The price of getting kyb and kyc verification wrong isn't just a slap on the wrist – it can be business-threatening. Regulators worldwide are increasingly willing to impose substantial penalties on companies that fail to meet their obligations, and these consequences extend far beyond just writing a check.

Take the case of Bancrédito International Bank & Trust Corporation, a Puerto Rico-based institution that learned this lesson the hard way. In September 2023, FinCEN imposed a $15 million civil money penalty against the bank for various regulatory violations, including failure to maintain an adequate AML program.

One particularly striking example from Bancrédito's case involved an investment company whose sole stated purpose was owning a luxury yacht. Despite never confirming who actually owned this yacht, the bank allowed the customer's account to process $1.3 million in suspicious transfers. This failure to properly conduct KYB verification – specifically identifying the ultimate beneficial owner – directly contributed to the massive fine.

But financial penalties are just the beginning. Reputational damage often proves even more costly in the long run. News of regulatory failures spreads quickly in today's connected world, eroding customer trust and damaging relationships with partners and stakeholders.

Legal action represents another serious risk. Companies and their executives can face both civil and criminal charges, depending on the severity of the violations. In extreme cases, operational restrictions may be imposed – regulators might limit business activities or even revoke operating licenses entirely.

The message is clear: robust kyb and kyc verification isn't just about regulatory compliance – it's an investment in your business's future stability and credibility. The cost of getting it right is always less than the cost of getting it wrong.

While the importance of kyb and kyc verification is undeniable, implementing these processes effectively isn't always straightforward. Many businesses find themselves wrestling with operational problems that can turn what should be routine compliance into a frustrating maze of complexity. The good news? These challenges aren't impossible, and with the right approach, we can transform cumbersome verification processes into smooth, efficient systems.

From my years of experience in due diligence, I've witnessed how even well-intentioned businesses can struggle with verification challenges. These obstacles don't just create headaches for compliance teams—they can expose companies to serious risks if left unaddressed.

Complex ownership structures top the list of challenges we encounter regularly. Compliance analyst who described dealing with "multiple layers, the seemingly random presence of holding companies, dotted and solid lines of indirect ownership"? They weren't exaggerating. Solveing corporate structures to identify Ultimate Beneficial Owners can feel like solving a puzzle where the pieces keep changing shape. International holding companies, trust arrangements, and shell entities create layers of complexity that require specialized expertise to steer effectively.

Data availability and reliability present another significant hurdle. Government registries might be outdated, fragmented across different agencies, or simply difficult to access. When businesses rely on manual processes or paper-based systems, the risk of working with stale or inaccurate information increases dramatically. This data uncertainty can leave companies vulnerable to fraud or compliance gaps.

Cross-border complexities multiply these challenges exponentially. Each jurisdiction brings its own regulatory requirements, language barriers, and data sources. What works perfectly for verifying a UK company might be completely inadequate for a business registered in Singapore or Brazil. Maintaining consistent verification standards across multiple countries requires deep knowledge of local regulations and access to diverse information sources.

The danger of cybersecurity breaches adds another layer of concern. As verification processes become increasingly digital, protecting sensitive customer and business information becomes paramount. Companies must balance accessibility with security, ensuring their systems are both user-friendly and fortress-strong against cyber threats.

Manual errors and resource constraints create ongoing operational challenges. Human-driven processes are inherently prone to mistakes—a missed detail here, a data entry error there, or inconsistent application of policies can create compliance gaps. These manual processes also demand significant time and staffing resources, straining budgets and limiting scalability.

Perhaps most frustratingly, businesses struggle to balance compliance rigor with customer experience. Nobody wants to subject legitimate clients to endless document requests or lengthy onboarding processes. Yet cutting corners on verification can expose businesses to regulatory penalties and reputational damage.

The challenges are real, but they're not impossible to overcome. Through careful planning and smart implementation, businesses can create kyb and kyc verification processes that are both thorough and efficient.

A risk-based approach forms the foundation of effective verification. Not every customer or business presents the same risk level, so why treat them all identically? By categorizing clients as low, medium, or high risk, companies can apply appropriate levels of scrutiny. Standard due diligence works fine for straightforward cases, while Improved Due Diligence kicks in for higher-risk situations. This targeted approach optimizes resources while maintaining security.

Technology and automation offer transformative benefits that I've seen revolutionize verification processes. Automated systems can achieve 90% faster onboarding compared to manual processes, while reducing client touchpoints by 93% and cutting KYC costs by 95%. These aren't just impressive statistics—they represent real improvements in efficiency and accuracy.

Automated solutions provide real-time access to global databases and registries, ensuring verification checks use the most current available information. They eliminate human error in data processing and can scale seamlessly as business volumes grow. Most importantly, they free up human resources to focus on complex cases that genuinely require investigator expertise.

Centralized data management creates a single source of truth for all verification information. Instead of scattered files and duplicate processes, everything flows through one integrated platform. This consolidation improves consistency, reduces redundancy, and makes it easier to track compliance across the entire organization.

Staff training remains crucial even with advanced technology. Team members need thorough understanding of regulatory requirements, risk assessment methodologies, and proper use of verification tools. Well-trained staff ensure that processes are applied correctly and consistently, catching issues that automated systems might miss.

Frictionless onboarding doesn't mean sacrificing security—it means designing processes that are both robust and user-friendly. Clear communication, intuitive interfaces, and streamlined workflows help legitimate customers complete verification quickly while maintaining thorough security checks.

Continuous monitoring integration ensures that verification doesn't end at onboarding. By building ongoing monitoring directly into the verification process, businesses can detect changes in risk profiles and suspicious patterns proactively, rather than reactively.

The key is finding the right balance between thoroughness and efficiency. For businesses dealing with complex verification challenges, especially those requiring investigator-led analysis, partnering with experienced due diligence providers can make the difference between struggling with compliance and mastering it. You might find additional insights in our article on 5 Critical Reasons to Run Vendor Background Checks.

Throughout this guide, we've explored the essential world of kyb and kyc verification and why these processes have become non-negotiable for modern businesses. Think of KYC as your security checkpoint for individuals — carefully verifying who your customers really are through identity documents and risk assessments. Meanwhile, KYB acts as your detective work for businesses, solveing complex corporate structures to find the real people pulling the strings.

The numbers don't lie. With $10 billion in fines hitting banks in 2019 alone, and recent penalties like the $15 million fine against Bancrédito, the cost of getting these processes wrong is staggering. But beyond avoiding penalties, robust verification protects your business from becoming an unwitting accomplice to financial crime.

The challenges are real. Complex ownership structures can feel like solving a puzzle with missing pieces. Data scattered across jurisdictions makes verification feel like detective work. Manual processes create bottlenecks and errors that automated solutions can eliminate.

But the solutions are within reach. A risk-based approach lets you focus resources where they matter most. Automation can cut onboarding time by 90% while reducing costs by 95%. Continuous monitoring ensures your due diligence stays current as relationships evolve.

For straightforward cases, these best practices often suffice. However, when you're dealing with intricate international networks, opaque ownership structures, or high-risk scenarios that demand deeper investigation, technology alone may not be enough.

This is where investigator-led analysis becomes invaluable. At Business Screen, our Cleveland-based team of experts specializes in those complex cases that require human insight and global reach. We provide comprehensive, real-time reports that go beyond what automated systems can deliver, ensuring the highest level of due diligence for your most challenging verification needs.

Your business deserves protection from unseen risks. Take control of your risk with expert third-party due diligence and let our experienced investigators help you steer the complexities of kyb and kyc verification with confidence and precision.

.png)