Learn how private equity screens for lbo candidates. Uncover key financial metrics, market insights, and strategic opportunities.

How private equity screens for LBO candidates is a critical process that determines the success or failure of billion-dollar investments. Private equity firms use a systematic approach to identify companies that can handle significant debt loads while generating strong returns for investors.

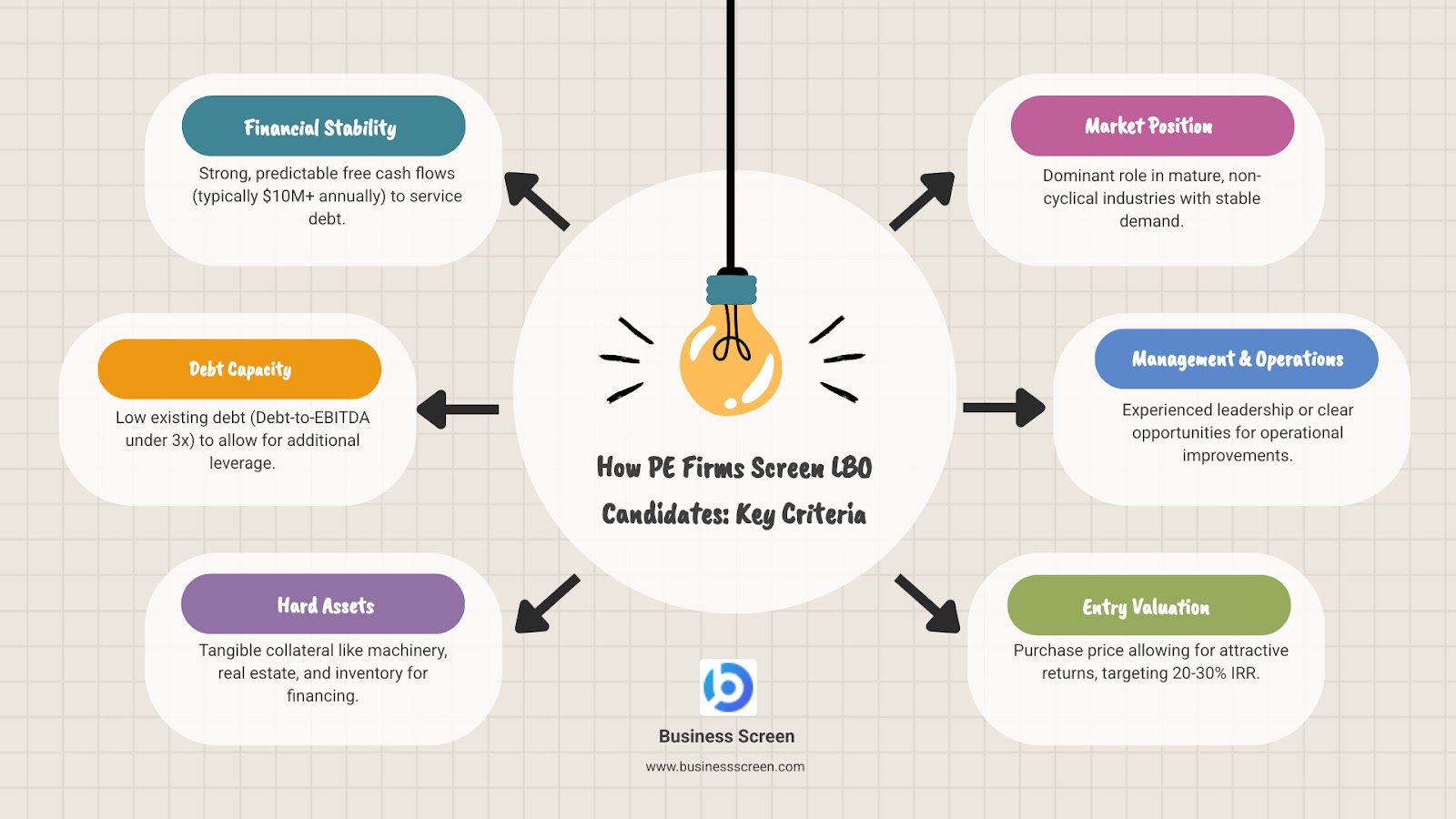

Quick Answer: The 8-Step LBO Screening Process

The stakes couldn't be higher. As one investment research report notes, "About 27% of the A-rated corporate index may be buyout targets," with recent deals ranging from $11 billion to $44 billion in size. With over 4,100 private equity firms competing for deals, the screening process has become increasingly sophisticated.

Today's LBO candidates look very different from the small, struggling companies of the 1980s. Modern private equity firms target well-managed, profitable businesses that can support leverage ratios of 5x EBITDA or higher while maintaining operational excellence.

I'm Ben Drellishak, and I've spent years helping businesses understand how private equity screens for LBO candidates through comprehensive due diligence and risk assessment. My work at Business Screen has given me deep insights into what makes companies attractive targets and what red flags cause deals to fall apart.

The leveraged buyout (LBO) gained prominence in the 1980s, thanks to pioneers like Jerome Kohlberg and Henry Kravis, founders of KKR. As its name implies, the use of financial leverage, or debt, is one of the primary elements distinguishing an LBO from a traditional acquisition. Leverage can improve equity returns to the sponsors, who have discretionary control over all cash flows that exceed the debt payments. This aggressive use of debt means that an LBO is only as strong as the company's ability to service that debt. This is why a meticulous screening process is not just important, it's absolutely essential.

So, what exactly are private equity firms looking for when they sift through thousands of potential targets? Let's dive deep into the criteria.

Think of how private equity screens for LBO candidates like a bank evaluating someone for a massive mortgage. The difference? We're talking about companies taking on debt that's often 5-7 times their annual earnings. That's why the financial foundation has to be rock-solid.

At the heart of every successful LBO is a simple truth: the company's cash flows will determine whether the deal thrives or dies. Private equity firms aren't just buying businesses – they're betting that these companies can generate enough cash to pay down mountains of debt while still growing and eventually delivering strong returns to investors.

The financial screening process focuses on three critical areas: steady cash flows, valuable hard assets, and low capital expenditure requirements. Companies that excel in all three areas become prime LBO targets because they can handle significant leverage without breaking under the pressure.

When private equity professionals dig into the numbers, they're looking for patterns that spell "reliable cash machine." The financial litmus test isn't just about profitability – it's about predictability and cash conversion.

Predictable revenue forms the bedrock of any LBO candidate. Think subscription-based businesses, essential services, or companies with long-term contracts. These revenue streams give lenders confidence that the money will keep flowing even during economic downturns. A software company with 95% customer retention rates looks far more attractive than a project-based consulting firm with lumpy, unpredictable income.

The magic happens when companies demonstrate strong cash generation capabilities. This means efficiently converting earnings into actual cash that can service debt. Companies with minimal working capital needs – those that don't tie up cash in inventory or wait months for customer payments – are particularly attractive. As financial experts note, free cash flow determines how much leverage a business can realistically support. You can learn more about calculating Free Cash Flow and why it's so crucial to LBO success.

EBITDA margins tell another important story. Steady or improving margins signal operational efficiency and pricing power. Since most LBO exits are based on EBITDA multiples, consistent margin performance directly impacts the eventual sale price. A company maintaining 20% EBITDA margins through various economic cycles demonstrates the kind of resilience that makes private equity firms excited.

The existing debt capacity analysis involves examining key ratios like debt-to-EBITDA and interest coverage ratios. Ideally, target companies start with relatively low debt levels, giving private equity firms room to add leverage without immediately stressing the business. The sweet spot? Companies that can comfortably handle 5-6x EBITDA in total debt while still covering interest payments with room to spare.

Beyond the pure cash flow metrics, the nature of a company's assets and its capital expenditure requirements can make or break an LBO opportunity.

Hard assets serve as the collateral that makes banks willing to lend at attractive rates. Machinery, inventory, accounts receivable, and especially real estate provide tangible security for lenders. Banks sleep better at night knowing they can recover their money through asset sales if things go sideways. This collateral support enables private equity firms to secure the massive debt financing that makes LBOs possible in the first place.

Real estate deserves special mention because it often appreciates over time while providing stable collateral value. Manufacturing companies with valuable facilities or retail chains with prime locations offer built-in security that financial services companies simply can't match. For deeper insights into evaluating real estate assets, our commercial real estate due diligence guide provides comprehensive coverage.

Low capital expenditure requirements represent the other side of the cash flow equation. Companies that don't need to constantly reinvest large portions of their cash flow into operations leave more money available for debt service. Private equity firms distinguish between maintenance CapEx (keeping the lights on) and growth CapEx (expansion investments).

The ideal LBO candidate has minimal maintenance CapEx requirements. A software company might need only 2-3% of revenue for maintenance investments, while a manufacturing company could require 8-10% just to maintain existing operations. This difference dramatically impacts how much cash remains available for debt payments and eventual returns to equity holders.

Companies that are "burning cash on experimental projects or massive facility upgrades" rarely make good LBO candidates, regardless of how exciting their growth prospects might seem. The debt service requirements of an LBO demand disciplined capital allocation and predictable cash generation above all else.

After establishing that a company has solid financial foundations, how private equity screens for LBO candidates shifts to examining the bigger picture. We need to understand where the business sits in its market, whether it can defend its position over time, and most critically, whether we can buy it at a price that makes sense.

Think of it this way: you might find the perfect house with great bones and steady rental income, but if you pay too much for it, your investment returns will suffer. The same principle applies to LBOs, where the interplay between market dynamics and valuation can make or break a deal.

When private equity firms evaluate potential targets, they're looking for businesses that operate in what we call "boring but beautiful" markets. These are mature markets with predictable patterns, stable customer demand, and limited surprises.

Non-cyclical industries are particularly attractive because their revenues don't swing wildly with economic ups and downs. Think about companies that provide essential services or products people need regardless of whether the economy is booming or struggling. Utilities, waste management, and certain healthcare services fall into this category. Their cash flows remain relatively steady, which is exactly what you want when you're counting on those cash flows to service debt.

The concept of high barriers to entry is crucial here. These barriers act like a protective moat around the business, making it difficult for new competitors to waltz in and steal market share. Brand recognition is one powerful barrier - customers often stick with brands they know and trust. Intellectual property like patents or proprietary technology can also keep competitors at bay.

Companies with high degrees of specialization often benefit from these natural defenses. When a business has spent years building expertise in a niche market, it becomes much harder for newcomers to replicate that knowledge and customer relationships overnight.

To properly assess a company's market position, we often rely on comparable companies analysis. This helps us understand how the target stacks up against its peers in terms of profitability, growth, and market share.

Here's where many promising LBO deals go wrong: paying too much upfront. Even if you find a company that checks every other box perfectly, overpaying at the entry can doom your returns from day one.

Valuation discipline isn't just a nice-to-have - it's absolutely essential. Private equity firms typically target returns of 20-30% IRR and want to multiply their invested capital by 2-3 times over a 3-5 year holding period. These ambitious targets require careful attention to what we call the entry multiple versus the exit multiple.

Let's say you buy a company at 8 times EBITDA (the entry multiple) and plan to sell it at 7 times EBITDA (the exit multiple) five years later. Even if you double the company's EBITDA through operational improvements, you're fighting an uphill battle because of that multiple compression. The math simply doesn't work in your favor.

This is why successful private equity firms focus on buying at a discount or at least at reasonable valuations. Sometimes the best opportunities come when an entire industry is temporarily out of favor, allowing you to acquire quality assets at attractive prices. The key is having the patience to wait for the right opportunity rather than chasing every deal that comes along.

As one industry expert puts it, "Even a perfect candidate can be a poor investment if overpaid for." Understanding What Makes a Good LBO Candidate? involves not just evaluating the company itself, but also being realistic about what price makes sense given your return expectations.

The most successful LBO investors are often those who can say "no" to deals that don't meet their valuation criteria, even when everything else looks attractive.

While financials and market position are foundational, the people running the company and the opportunities for strategic optimization are equally vital. Private equity firms aren't just passive investors; they actively seek to create value through both human capital and strategic improvements.

When how private equity screens for LBO candidates moves beyond spreadsheets, the human element becomes crucial. Think about it - you're betting hundreds of millions on a team's ability to execute under pressure while carrying significant debt. Management quality can make or break an entire deal.

We look for leaders who have proven they can steer challenges, grow businesses, and work collaboratively with PE partners. The best management teams understand that private equity isn't just about financial engineering - it's about operational excellence and strategic execution.

Succession planning presents some of the most attractive LBO opportunities in today's market. With Baby Boomers retiring in droves, many profitable businesses face a leadership vacuum. These situations create win-win scenarios where the retiring owner gets liquidity while the PE firm acquires a quality business, often at reasonable valuations.

Sometimes we encounter businesses with leadership gaps or underperforming management. Rather than walking away, experienced PE firms see opportunity. They can partner with industry veterans or facilitate a Management Buyout (MBO) where capable internal leaders team up with the PE firm to acquire the company.

At Business Screen, we understand that assessing management quality goes far beyond reviewing resumes. Our comprehensive background investigations help PE firms understand the full picture of leadership capabilities, integrity, and potential red flags. We believe in The Better Way to Conduct a Due Diligence Background Check on a New Business Partner to ensure you're partnering with the right people.

The most successful LBOs don't just rely on financial leverage - they create value through strategic change. Smart PE firms identify companies sitting on hidden value that can be open uped through targeted changes.

Non-core asset sales often provide immediate cash infusions while sharpening the company's focus. Many businesses, especially family-owned companies or conglomerates, accumulate assets over time that no longer fit their strategy. These assets can be sold to generate cash for debt reduction or reinvestment in core operations.

Forced divestitures create unique opportunities. When regulatory requirements or antitrust concerns force companies to sell divisions quickly, PE firms can often acquire quality assets at attractive prices. The urgency of these situations sometimes leads to favorable deal terms.

Spin-offs of underperforming divisions represent another value creation opportunity. A division that's dragging down the parent company's performance might thrive as a standalone entity under focused PE ownership. Smith & Wesson (Nasdaq: SWHC) announced that it is spinning off its security division, creating exactly this type of opportunity.

Operational improvements and cost-cutting initiatives can dramatically boost EBITDA and cash flow. PE firms excel at identifying inefficiencies in overhead, supply chain management, pricing strategies, and sales processes. These improvements directly impact the company's ability to service debt and generate returns.

The complexity of these strategic opportunities requires thorough investigation and planning. That's where comprehensive due diligence becomes essential. Our M&A Due Diligence: The Ultimate Guide & Checklist provides frameworks for evaluating these multifaceted value creation opportunities.

The beauty of strategic value creation is that it benefits everyone involved - the company becomes more efficient and focused, management gets better tools and resources, and investors see improved returns. It's this combination of financial discipline and strategic vision that makes the best LBO candidates truly shine.

For aspiring private equity professionals, understanding how private equity screens for LBO candidates isn't just theoretical knowledge—it's a skill you'll need to demonstrate under intense pressure. The LBO modeling test has become the ultimate proving ground in private equity recruiting, separating those who truly understand deal mechanics from those who only know the theory.

Think of it as the financial equivalent of a chess tournament with a ticking clock. You have all the knowledge, but can you execute flawlessly when every second counts? That's exactly what these tests are designed to measure.

Picture this: you walk into a conference room, sit down at a computer, and receive a case study packet. The clock starts ticking, and you have exactly 60 minutes to build a complete LBO model from scratch. No pressure, right?

These tests are essentially "Excel speed tests" that reveal whether you can quickly and accurately construct the financial framework that private equity firms use to evaluate deals. Some firms might ease you in with a paper LBO exercise first, but most jump straight to the digital deep end.

Here's the sobering reality: the median score is often below 50%. That's not because the concepts are impossibly difficult—it's because building a functional model under extreme time pressure requires both technical skill and mental composure.

The key components you'll need to master include transaction assumptions that outline the purchase price, debt structure, and equity contribution. You'll build a Sources & Uses schedule showing exactly where the money comes from and where it goes—think of it as the deal's financial blueprint.

Don't expect to build a full three-statement model in an hour. Instead, you'll focus on a streamlined Income Statement and partial Cash Flow Statement to calculate Free Cash Flow. The debt schedule becomes your lifeline here, projecting how various debt tranches get paid down while calculating interest expenses.

The ultimate goal is calculating returns—specifically IRR and MOIC. Private equity firms typically target IRRs between 20% and 30% with MOICs between 2x and 3x. Finally, you might need to create Sensitivity Analysis tables showing how returns change under different scenarios.

Success comes down to speed and accuracy. Forget about making your model look pretty—focus on getting the core calculations right. Every minute spent on formatting is a minute not spent on the mechanics that actually matter.

Want to see what you're up against? Check out this 60-Minute LBO Modeling Test – Case Study Prompt (PDF) to get a feel for the real thing.

My advice? Practice 5-10 modeling tests before stepping into that conference room. The concepts might be familiar, but executing them flawlessly under pressure is an entirely different challenge. This test isn't just about technical skills—it's about proving you can think like a private equity professional when it counts.

After years of helping clients steer the complex world of private equity due diligence, I've encountered these questions countless times. Let me share the insights I've gained from working with both PE firms and potential target companies.

If I had to pick just one factor that makes or breaks an LBO candidate, it would be a history of strong, stable, and predictable free cash flow. Everything else in the screening process essentially revolves around this core principle.

Here's why this matters so much: how private equity screens for LBO candidates always comes back to debt service capability. When a PE firm loads a company with 5x or 6x EBITDA in debt, that company needs to generate consistent cash to make interest payments, pay down principal, and still have enough left over for operations and growth.

I've seen deals fall apart because companies had impressive revenue growth but couldn't convert those sales into actual cash. Revenue that gets tied up in accounts receivable or inventory doesn't help when debt payments are due. That's why PE firms dig deep into working capital cycles and cash conversion patterns during their screening process.

This is where many entrepreneurs get confused, and the short answer is typically, no. While high-growth tech companies might seem attractive because of their potential, they're usually terrible LBO candidates for several practical reasons.

PE firms prefer mature, non-cyclical industries with predictable demand patterns. High-growth tech companies are the opposite of what PE firms want. They usually require massive ongoing investment in research and development, have unpredictable cash flows, and operate in rapidly changing markets where today's leader can become tomorrow's has-been.

Think about it this way: if a software company needs to spend 30% of its revenue on R&D just to stay competitive, that's 30% less cash available for debt service. These companies are much better suited for venture capital, where investors expect to fund growth rather than extract cash.

The exception might be a mature tech company with a dominant market position, predictable subscription revenue, and minimal reinvestment needs. But even then, PE firms approach tech deals very carefully.

The evolution of LBO targets tells a fascinating story about the maturation of private equity as an asset class. When I started in this business, the stereotypical LBO target was a small, struggling company that could be bought cheap and fixed up.

Historically, LBOs targeted smaller, underperforming companies - think family businesses with outdated operations or divisions being spun off from larger corporations. The strategy was simple: buy low, improve operations, and sell high.

Today's reality is dramatically different. With massive PE funds managing hundreds of billions in capital, even large, A-rated, and well-managed corporations can become targets. We're talking about companies with billions in revenue and thousands of employees.

What hasn't changed is the fundamental requirement: these companies still need the capacity to take on more debt and offer clear opportunities for operational optimization. The difference is that today's PE firms are sophisticated enough to identify value creation opportunities in already well-run businesses.

Modern LBO candidates might be profitable companies that can benefit from digital change, international expansion, or buy-and-build strategies. The screening process has become more nuanced, looking for companies that are good but could be even better with the right capital and expertise.

This evolution reflects the professionalization of private equity and the enormous amounts of capital seeking attractive returns in today's market.

Understanding how private equity screens for LBO candidates is like watching master detectives at work. They methodically examine every clue - from cash flow patterns to management capabilities - before making their move. This isn't a simple checklist exercise; it's a sophisticated blend of number-crunching and gut instinct.

The screening process reveals four critical pillars that determine success. Financial stability forms the foundation, with firms demanding predictable cash flows that can handle significant debt loads. Market position comes next, as companies in mature industries with high barriers to entry offer the stability private equity craves. Management quality can make or break a deal - even the most attractive financial metrics won't save an investment if leadership can't execute the plan. Finally, strategic potential separates good deals from great ones, as savvy firms spot opportunities to open up hidden value through operational improvements or asset sales.

What makes this process fascinating is how it balances cold, hard analysis with human judgment. A spreadsheet might show perfect EBITDA margins, but if the management team lacks succession planning or the industry faces disruption, experienced investors know to walk away. Conversely, they might see opportunity where others see problems - perhaps a temporary downturn has created an attractive entry price, or aging leadership presents a chance to install fresh talent.

The stakes justify this thorough approach. With deals now reaching tens of billions of dollars, private equity firms can't afford to get the screening wrong. A single mistake in candidate selection can wipe out years of returns across multiple investments.

For private equity firms, this rigorous vetting represents just the beginning of their value creation journey. Once they've identified the right target at the right price, the real work of change begins. But without proper screening upfront, even the most skilled operational improvements won't deliver the 20-30% IRR returns that investors expect.

At Business Screen, we see how critical this initial assessment phase becomes. Our investigator-led approach helps private equity firms dig deeper into the human elements that numbers alone can't reveal. Whether it's verifying management credentials or uncovering potential red flags, thorough due diligence transforms good screening into great investments. Learn more about our investment due diligence services to strengthen your investment strategy from day one.

.png)