What Borrowers Can Hide When Lenders Screen for Speed

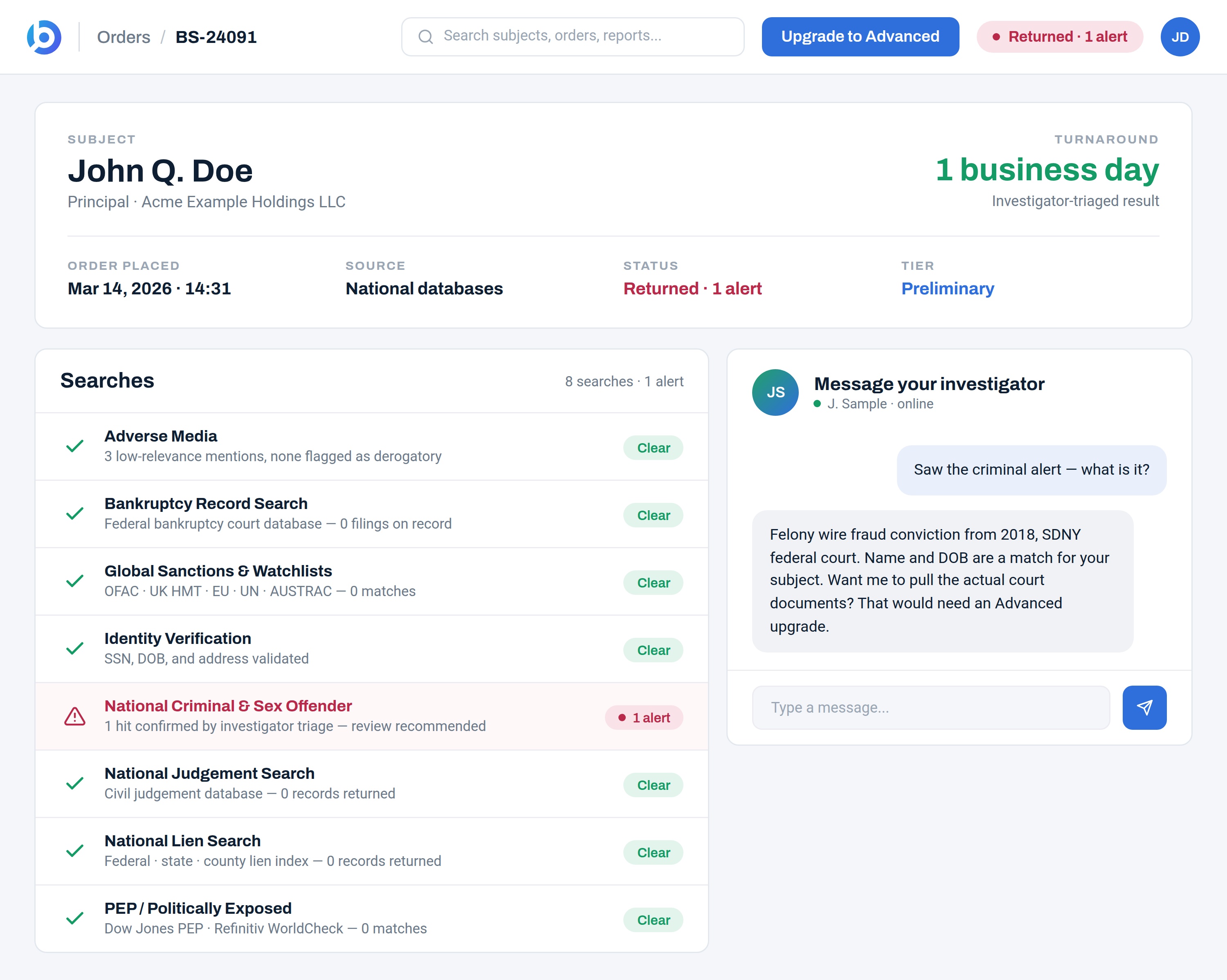

Speed determines who wins the deal, and some borrowers take advantage of it. Clean applications can mask undisclosed tax liens, active litigation, or regulatory actions that haven’t reached aggregated databases. For underwriting teams relying on standard commercial due diligence services, the gap between what’s been filed and what’s searchable is where exposure builds.

When limited partners and investors require defensible business due diligence as part of their reporting, a database check alone is not a sufficient answer. The question is whether your screening catches what matters before capital is committed.