A company is about to run a screen on the guarantor behind a deal, and someone on the team pauses to ask whether they need a signed authorization first. For business diligence, the answer is no. A non-FCRA background check does not require the subject's consent when it informs a business decision.

The confusion usually traces back to one assumption, that the Fair Credit Reporting Act, or FCRA, is the rulebook behind background checks in general. It is not. Whether you need consent for a background check depends on the purpose the report serves, and business due diligence is not one of the consumer decisions the Act governs.

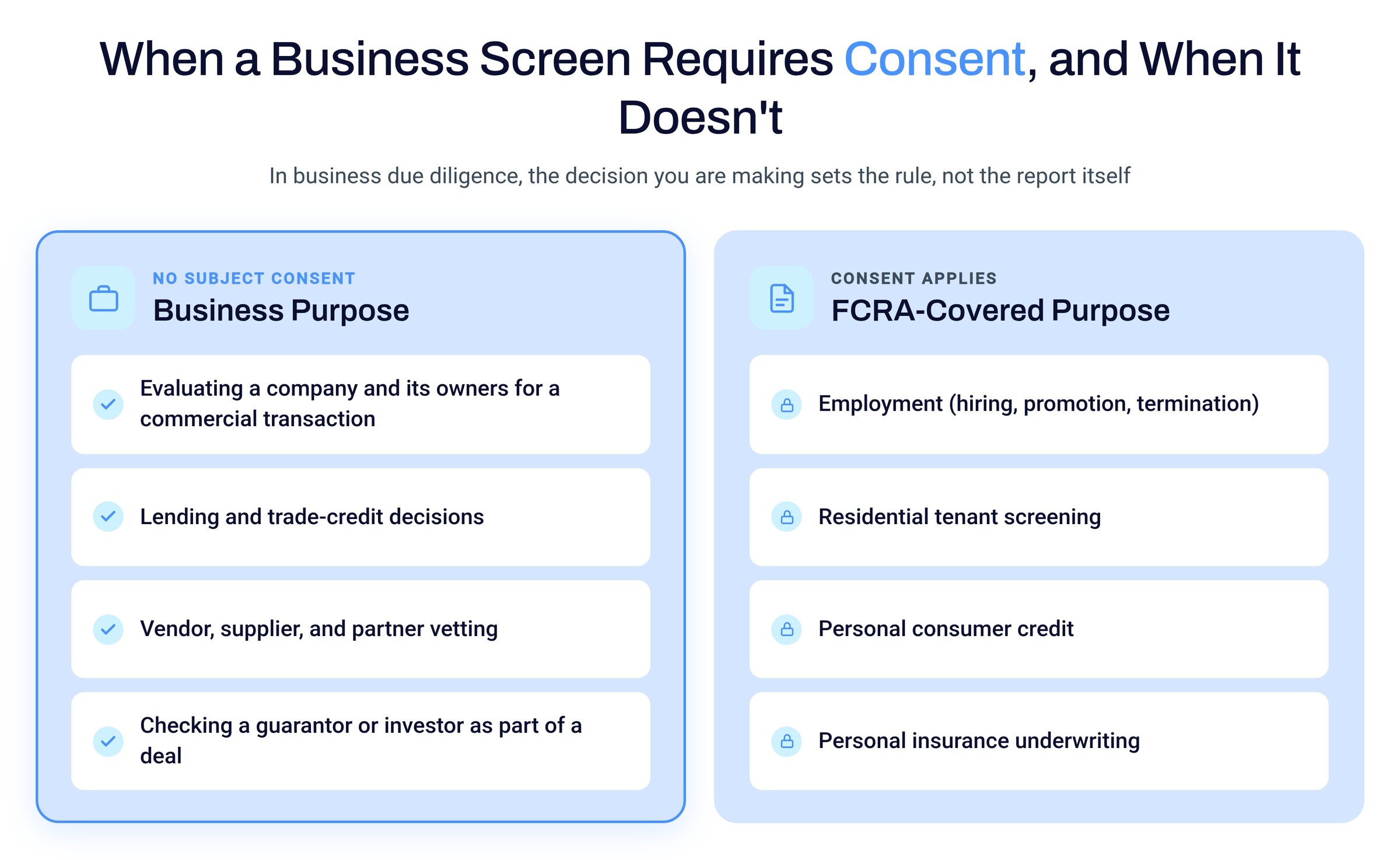

FCRA covers a specific set of decisions about people in their private lives, employment such as hiring and promotion, residential tenant screening, personal consumer credit, and personal insurance underwriting. When a report informs one of those, the Act's requirements attach, which means a permissible purpose, written authorization from the subject, an adverse-action notice, dispute rights, and a provider registered as a Consumer Reporting Agency (CRA).

Business due diligence is not on that list. Evaluating a company, its owners, or its principals for a commercial transaction is not a decision about someone as a consumer, so it does not carry those obligations.

Because a report built for a business decision is not a consumer report, and the provider is not a Consumer Reporting Agency, the consent form and the adverse-action process do not apply. You do not need the subject's authorization to screen a company and the people who run it for a commercial purpose. That is the premise behind non-FCRA due diligence, gathering what a business decision calls for without the consumer-reporting machinery attached to it.

The absence of a consent step is a practical advantage. Diligence starts without waiting on a signature, and in a suspected-fraud or adversarial situation you are not tipping off the subject. In many cases you can also see the financial-stability signals that matter, such as liens and judgments, through public records, without pulling anyone's personal credit.

That freedom comes with a firm limit. Because a non-FCRA report is built for a business decision, it can be used only for a legitimate business purpose, not to reach a conclusion about a person as a consumer.

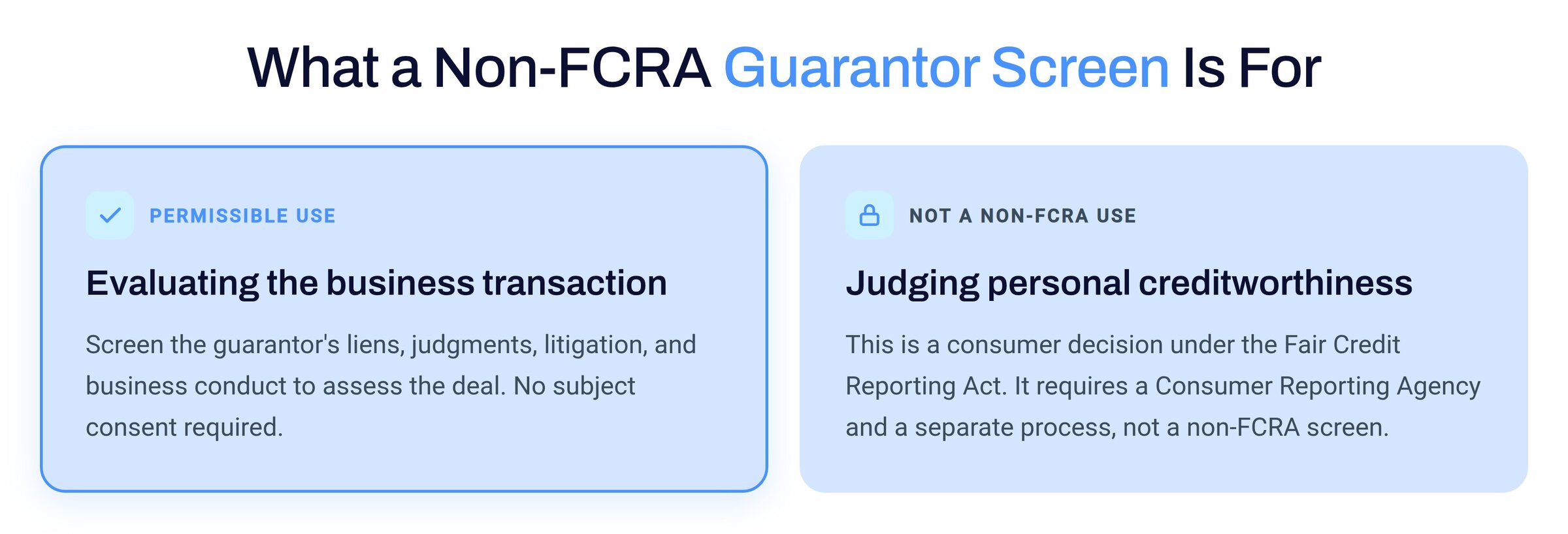

The guarantor is the clearest case. You can screen a guarantor to evaluate the business transaction, and their liens, judgments, litigation, and business conduct are fair game for that decision. What you cannot do is use that same screen to judge the individual's personal creditworthiness. That is a consumer-credit decision, it falls under the Fair Credit Reporting Act, and it belongs to a Consumer Reporting Agency, not a non-FCRA screen. The purpose sets the boundary, and the boundary does not move.

Much of what business teams screen sits comfortably inside that line, without a consent step, because the decision is about a business relationship rather than a person's private life. A commercial background check on a company and the owners or guarantors behind it is a business purpose, whether you are extending commercial credit, onboarding a vendor or partner, or weighing an investment. It is also why a thorough screen reaches the principals, not just the entity on paper, since the people are usually where the real risk sits.

If a decision ever turns into an employment, tenant, or personal-credit call, it goes to a provider registered as a Consumer Reporting Agency instead. Within the business lane, the depth is yours to set, from a fast automated lookup on routine work to an investigator-verified report when the stakes justify it.

A few checks are the exception to the no-consent rule, and the reason is the source of the records, not the Fair Credit Reporting Act. An international search on an individual requires the subject's consent along with a government-issued ID, because foreign data-protection rules and the overseas record sources set that condition before anything can be pulled.

Some verifications work the same way for a practical reason. Confirming a person's education or employment history relies on details only the subject can supply, the schools and dates or the employers and dates, and those records come back through the subject's cooperation rather than from open public files. None of this shifts the FCRA line. It reflects where the information lives and what a source needs before it will release it.

So, does a non-FCRA background check require consent? For business due diligence, no. Consent follows the purpose of the decision, not the label on the report. As long as the screen serves a business decision about a company, its owners, or its guarantors, it stays outside the consent requirement, and it stays there because the business side is the only place a non-FCRA report belongs.

As a non-FCRA, investigator-supported provider, we help teams keep that line clean and right-size the diligence behind it. If you want to talk through whether a screen fits a permissible business purpose, or how much depth a counterparty warrants, fill out the form below and our investigators will follow up.

.png)